ETFs and index funds outperform most actively managed investments. That's impressive, but there's an instrument out there that's better than an ETF for most investors: the Direct Index.

A Direct Index is a basket of stocks that tracks an index. The difference between a Direct Index and an ETF or an Index Mutual Fund is that with a Direct Index the investor directly owns the underlying shares. The simplest Direct Index, at least conceptually, is a basket that contains all the securities in the underlying index. With the S&P 500, that would mean a basket of, well, 500 stocks. For some investors, this may be fine, but for most it’s a bit burdensome, especially with larger indexes like the Wilshire 5000. Therefore, Direct Indexes are usually just a representative sample of the full index, say 50 or 100 stocks that track the S&P 500.

The Advantages of Direct Indexes

There are three main advantages to Direct Indexes: Tax efficiency, Risk customization and ESG customization.

- Tax Efficiency. ETFs are tax-efficient. Direct Indexes are more tax-efficient. Our tests show that relative to an ETF, Direct Indexes add more than 1% per year in higher after-tax returns. This is the primary advantage of Direct Indexes, and it’s worth looking at in some detail.

- Tax loss harvesting. If you purchase an ETF and its underlying index goes up in value, you can’t do any loss harvesting. But even though the index went up, it’s likely that some of the individual shares went down. With a Direct Index, you can sell those individual losers.

- Gains deferral. If you sell an ETF, you’re effectively selling every share of the underlying index pro rata. With a Direct Index, you can selectively avoid selling the top gainers.

To test how much a Direct Index benefits from these tax advantages relative to an ETF, we did a five-year backtest of a sector-rotation strategy implemented with ETFs vs Direct Indexes. The Results: the Direct Indexes added 1.93% per year in tax alpha:

Five Year Tax-managed Sector Rotation Strategy using Direct Index vs ETF

Annualized % Cumulative % Change in

Pre-Tax Returns0.06% 0.28% Change in

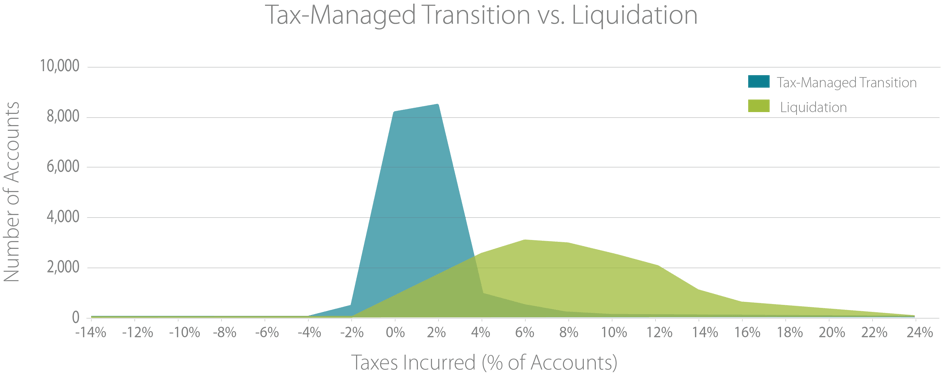

After-Tax Returns1.98% 10.28% Tax Alpha 1.93% 10.01% - Transition. Imagine you want to transition a legacy equity portfolio into an index. If you invest in an ETF, you’ll have to start by liquidating your existing holdings. With a Direct Index, you can incorporate some of your current holdings into your Direct Index portfolio. The only trades you need to make are those required to reduce concentrations and fill in missing sectors. The difference in tax efficiency is striking. We compared the tax impact of these two strategies for 18,000 actual investor equity portfolios. The difference? Liquidation would cost investors an average of 7.21% of portfolio value in taxes. Transitioning to a Direct Index in a tax-sensitive manner (as implemented using our tax-management transition analytics) would cost an average of only 0.29% of portfolio value. Here’s the graph:

- Risk Customization. Suppose you work in the energy sector and you’d therefore like to underweight energy in your portfolio. You can’t do that with a broad-index ETF — you can’t ask for SPY minus the energy sector. But you can do it with a Direct Index. Like all separately managed accounts, the holdings can be customized to meet individual investor needs.

- ESG/Social Criteria customization. The same story applies to ESG constraints. You can’t ask for SPY minus tobacco stocks and firms with poor governance records. You can with a Direct Index.

The market for wealth management services is moving away from a “beat the benchmark” value proposition. In its place, investors will demand more value, which includes tax management, risk customization and impact investing.

The technological advances behind mass market Direct Indexes

There’s a back-to-the-future quality to Direct Indexes. Owning baskets of stocks long predates the invention of the mutual fund or the ETF. Direct Indexes themselves have existed for decades. What’s new is that while Direct Indexes used to make sense only for ultra wealthy investors, they're now affordable and practical for ordinary investors. That is, what’s new isn’t the concept of Direct Indexes. It’s that they can now be offered at a price point that makes them a superior alternative to ETFs for most investors. The technological innovations that have made this possible include:

- Lower transaction costs. Bid/ask spreads and commissions are 1/10 or 1/100 of what they were 30 years ago. Baskets of stocks were prohibitively expensive for most investors. Large players, like mutual fund companies, used to have a large advantage over individual investors in executing trades at low cost. Now, this is sometimes reversed; individual investors, who don’t need to worry about moving the market, can now sometimes get better execution than mutual fund companies. We’re seeing commissions less than $.01/share, and we’re seeing trading and custody packaged for under 4 bps.

- Rebalancing automation. The tax and customization advantages of Direct Indexes are impressive, but they’re not automatic. You’ve got to actively manage a Direct Index portfolio to get tax savings and implement constraints. Traditionally, this was done by a highly compensated portfolio manager. But with sophisticated rebalancing systems (like, well, ours) these tasks can now be automated.

- Fractional shares. For portfolios smaller than $50,000, the need to buy whole shares can distort Direct Index portfolios, resulting in excess tracking error to the target benchmark. Multiple brokers offer fractional-share trading, making it technically feasible to manage and rebalance Direct Indexes portfolios to investors with as little as $50.

The Future of Direct Indexes

Smartleaf software is used to rebalance Direct Indexes, and this gives us a front row seat to the emerging trend of Direct Index mass-market distribution. We’re seeing interest from both wealth management firms, which use Direct Indexes as low-cost core portfolios, and from asset management firms that are gearing up to offer Direct Indexes as, effectively, products.

The case for Direct Indexes is pretty simple. ETFs are good. Direct Indexes are better. Is it time for you to go Direct?

COMMENTS